Opening a Stocks and Shares ISA: My Experience as a Beginner Investor

INVESTING · REAL WORLD

Opening a Stocks and Shares ISA was something I had thought about for years, but I never fully committed until I understood how useful it could be for long-term investing and tax-efficient wealth building.

For me, I had known about Stocks and Shares ISAs for a while, but I never really understood them enough to fully commit to opening one.

That changed once I started learning more about how they work, especially from the point of view of someone who already trades. I already had experience using a trading account, buying and selling positions, and taking on risk. But I wanted something separate from that. Something more long-term, more tax-efficient, and more focused on building wealth slowly over time.

This is what led me to open a Stocks and Shares ISA.

Summary

- I opened a Stocks and Shares ISA because I wanted a tax-efficient way to invest for the long term.

- I chose Trading 212 because there are no account, custody or commission fees on the Invest and ISA accounts.

- The account was opened online and I was investing within about 30 minutes.

- I started with £200 and set up a regular £200 monthly contribution.

- My ISA is mainly invested in VUAG because I want a simple buy-and-hold investment.

- I keep my ISA separate from my eToro trading account because they have completely different purposes.

Interested in index funds?

Read my beginner guide to index funds

Why I Decided to Open a Stocks and Shares ISA

The main reason for me was tax efficiency.

In the UK, you can currently put up to £20,000 per tax year into ISAs. This allowance can be split across different types of ISA, including Cash ISAs and Stocks and Shares ISAs.

Personally, I think the big attraction with a Stocks and Shares ISA is that capital gains, dividends and interest inside the ISA are sheltered from UK tax.

For me, the ISA is not for short-term trading. It is for buying, holding, and letting the money build over time.

That made a lot of sense to me. I already use a trading account, but I wanted to separate short-term trading from long-term investing. My trading account is more active. The ISA is for long-term wealth building.

Why I Chose Trading 212

I chose Trading 212 for my Stocks and Shares ISA.

The main reason was cost. Personally, I did not want a managed account and did not want to pay ongoing management fees if I could avoid it. I wanted something simple where I could choose my own investments.

Trading 212 appealed to me because there are no account, custody or commission fees on the Invest and ISA accounts. There can still be costs, such as a 0.15% foreign exchange fee when buying assets in another currency, but for what I wanted, it seemed like a good fit.

I wanted control over what I invested in, without paying someone else to manage the account for me.

I had also already used other trading platforms, so I was comfortable with the idea of managing investments myself.

Opening the Account

The process was much easier than I expected.

Within about 30 minutes, I had opened the account, completed the identification checks, added money, and started investing.

The whole process was online. The ID checks were straightforward and I did not run into any issues. This was one of the things that surprised me most. I think I had built it up in my head as something more complicated than it actually was.

The only part that took a little bit of getting used to was the interface.

I am used to eToro, so Trading 212 looked and felt different at first. But after placing a few orders and looking around the app, it became fairly straightforward.

How I Funded the ISA

I started fresh with the ISA rather than transferring from another account.

The initial deposit was £200 from my bank account, and I then set up a regular monthly contribution of £200.

For me, this was more important than trying to start with a huge amount. I wanted to get the account opened, get into the habit, and build from there.

Getting close to the full £20,000 ISA allowance is unlikely for me at the beginning, but that is not really the point right now.

The important part for me was starting the habit. Even if the amount is small at first, it gets the process moving.

What I Invested In

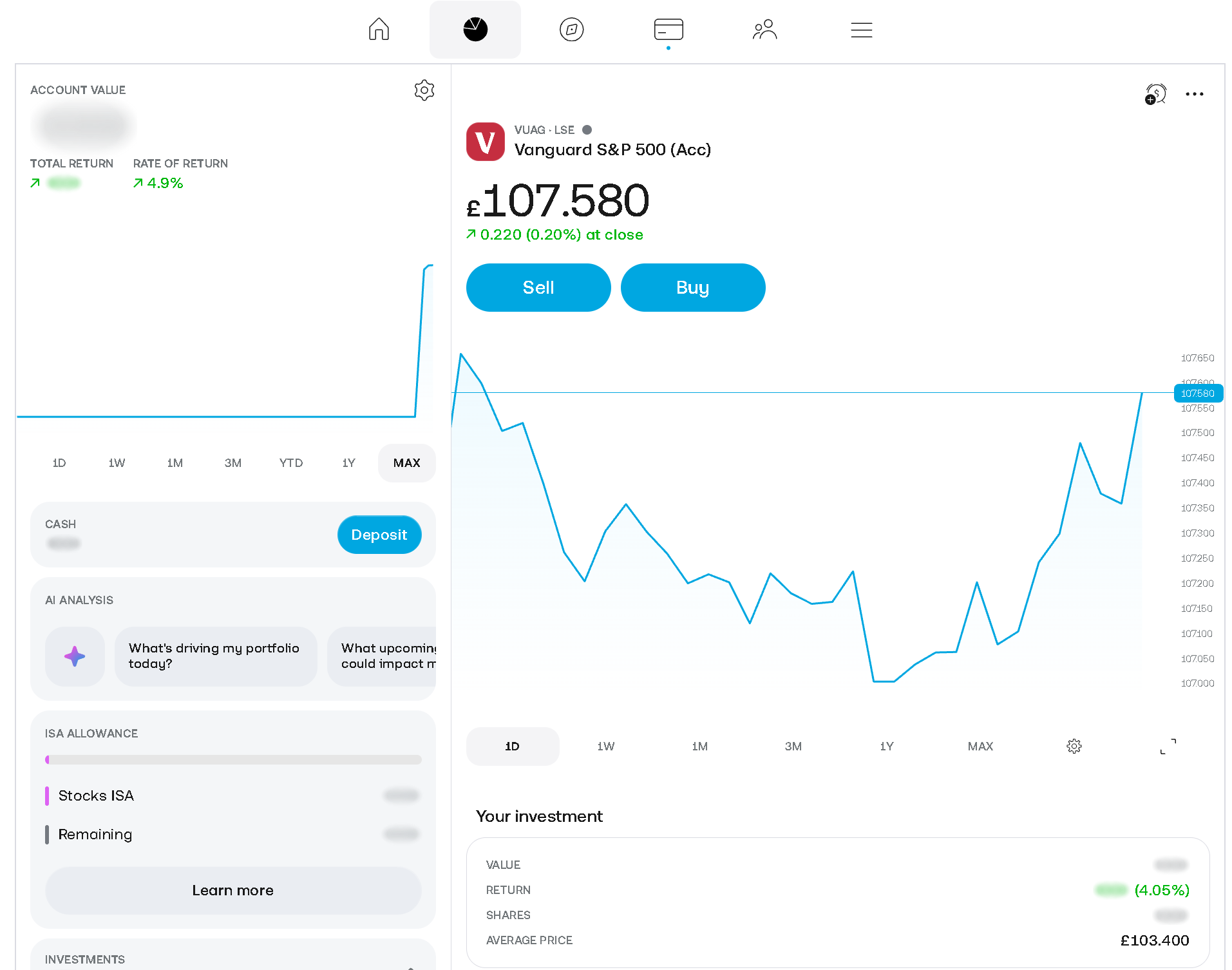

At the moment, my ISA money is invested in VUAG.

VUAG is Vanguard’s S&P 500 UCITS ETF accumulating version. Because it is an accumulating ETF, dividends are not paid out to me as cash. They are reinvested inside the fund.

That suits what I want from the ISA.

I am not using the ISA for short-term trading. It is being used to buy and hold for years. My plan is to keep investing regularly and let it build naturally over time.

Want to know why I chose VUAG?

Read why I invest in VUAG

How This Is Different From My Trading Account

This is probably the biggest difference for me.

I use my eToro account for active trading, mainly forex and some crypto. My ISA is different because it is focused on long-term investing rather than short-term trades.

Personally, I prefer the eToro interface for trading, especially with CFDs. I find the leverage, stop loss, margin and position details a bit more obvious there. That is just personal preference though, not really a criticism of Trading 212 or the ISA.

The ISA has a completely different purpose.

My trading account might hold a position for less than a day, whereas my ISA investments are intended to be held for years.

Keeping the accounts separate helps me keep the strategies separate. The trading account is for active trading. The ISA is for long-term investing.

I also like keeping them separate for tax reasons. My trading account is not sheltered from tax, whereas the ISA is. By keeping my long-term investing inside the ISA, it makes things simpler for me.

My Long-Term Plan

My plan is simple:

- Keep adding money regularly

- Stay invested for the long term

- Use the ISA for ETFs and long-term growth

- Keep active trading separate

- Increase contributions as bills reduce over time

I plan to keep investing for the rest of my life now.

As I get older and the bills come down, I would like to shift more spare cash into the ISA. Anything left after that can go into my trading account.

What I Wish I Had Known Earlier

The main thing I wish I had known is how simple it actually was to open one.

I hear people asking when the right time is to start investing. My honest answer would be: now.

That does not mean throwing thousands in without understanding the risks. It could be £50, £100, or even small amounts here and there. The important part is getting started and building the habit.

A Cash ISA may feel more reliable, and it has its place, but for me, the potential gains from investing are more attractive over the long term. I know the value can go down as well as up, and I am comfortable with that because I am thinking in years rather than weeks or months.

Important: investing is not risk-free. The value can go down as well as up, and you need to be comfortable with that before putting money into the market.

My Advice for Beginners

My advice would be to keep it simple.

Pick one broad index fund or ETF, invest regularly, and do not open the app every day.

That last part is important. If you check it constantly, every dip feels bigger than it probably is. Markets have bad years. That does not automatically mean the plan is wrong.

For me, the idea is to let the average returns work over a long period of time. I do not want to panic because of one bad year and take the money out at the wrong time.

The strategy only works if I actually stick to it. For me, that means investing regularly and not reacting emotionally to every market movement.

How It Has Performed So Far

So far, my ISA is up around 4.9%.

That is below the long-term average for the market, but it is still more than I believe I would have got from a Cash ISA over the same period.

More importantly, I am not really judging it over a short period. This is a long-term account for me. The aim is not to make quick money. The aim is to build wealth slowly and consistently.

Final Thoughts

Opening a Stocks and Shares ISA has been one of those things I wish I had done earlier.

I am an engineer trying to build wealth and create more stability for my family. With the cost of living, bills, tax and everything else going on, it can feel like a bit of a shambles at times. For me, the ISA is one practical way to start doing something about it.

It is not exciting or a get-rich-quick scheme. There is a difference between this and trading. For me, it is a simple, tax-efficient way to invest regularly and hopefully build something meaningful over time.

My trading account and my ISA will stay separate. The trading account is for active trading. The ISA is for long-term investing.

That separation makes sense to me, and it helps keep the purpose of each account clear.

If you are thinking about opening a Stocks and Shares ISA, my personal view is that starting small is better than not starting at all. Even if it is the minimum deposit and small regular amounts after that, it gets the habit going.

Just understand the risks, do your own research, and remember that investments can go down as well as up.

New to investing?

Start with my index funds for beginners guide

FAQs

What is a Stocks and Shares ISA?

A Stocks and Shares ISA is a UK investment account that lets you invest in things like shares, funds, ETFs and investment trusts. The main benefit is that capital gains, dividends and interest inside the ISA are sheltered from UK tax.

How much can I put into a Stocks and Shares ISA?

For the 2026/27 tax year, the total ISA allowance is £20,000. This is across all ISAs combined, not £20,000 for each type of ISA, according to the official GOV.UK ISA guidance.

Can I withdraw money from a Stocks and Shares ISA?

Yes, you can usually withdraw money from a Stocks and Shares ISA, but you may need to sell investments first. If the market is down when you sell, you could take a loss. Whether you can replace withdrawn money without affecting your allowance depends on whether your ISA is flexible.

Is a Stocks and Shares ISA better than a Cash ISA?

It depends on your goals and risk tolerance. A Cash ISA is generally lower risk, but the returns may be lower. A Stocks and Shares ISA carries investment risk, but it may offer better long-term growth potential.

What did I invest in first?

I started with VUAG, an accumulating S&P 500 ETF from Vanguard. I chose this because I wanted a simple long-term investment rather than picking lots of individual shares inside the ISA.

Do I still use my trading account?

Yes. I still use my trading account for active trading, mainly forex and some crypto. I keep this separate from my ISA because the ISA is for long-term investing.

Is this financial advice?

No. This is only my personal experience. I am not a financial advisor. Speak to a qualified professional if you are unsure what is suitable for your own situation.

Leave a Reply